What normally occurs in a bonafide real estate sale

INTRODUCTION – Real Estate Sales Legal Overview

Real Estate Sales Legal Overview – While there are many different factors in any real estate sale, there are certain common procedures and steps involved in most transactions. This is a birds-eye view of a typical sale but is by no means a comprehensive checklist of everything involved. It is up to the brokers and or attorneys involved to make sure everything is taken care of properly. Most real estate sales in California involve the use of California Association of Realtors (CAR) standard forms which are widely recognized. Over the last 100 years, there have been thousands of court cases involving real estate disputes and contracts and as a result the law and the forms are pretty well defined and established. A licensed California real estate broker or real estate attorney has access to those forms and should be familiar with them.

Subtitle: Pull out tax free gain while downsizing

Subtitle: Pull out tax free gain while downsizing

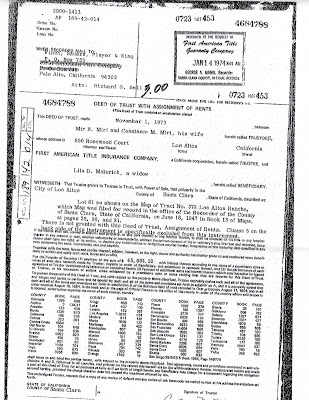

Real estate property ownership is legally changed by a document commonly known as a deed which is signed by the person making the ownership transfer. The deed is then recorded with the County recorder in the county where the property is located.

Real estate property ownership is legally changed by a document commonly known as a deed which is signed by the person making the ownership transfer. The deed is then recorded with the County recorder in the county where the property is located.