What is a Qualified Domestic Trust?

A Qualified Domestic Trust (also known as a “ QDOT”) is type of trust established where estate property passes to a non-U.S. citizen spouse to allow a marital deduction on the death of the first spouse. A QDOT allows the amount transferred into the Trust to qualify for the estate tax marital deduction. Without a QDOT, assets transferred from a decedent to a spouse who is a non-U.S. citizen do not qualify for the marital deduction on the decedent’s Federal Estate Tax return, form 709, and thus get taxed on the death of the spouse who is a U.S. citizen.

A Qualified Domestic Trust (also known as a “ QDOT”) is type of trust established where estate property passes to a non-U.S. citizen spouse to allow a marital deduction on the death of the first spouse. A QDOT allows the amount transferred into the Trust to qualify for the estate tax marital deduction. Without a QDOT, assets transferred from a decedent to a spouse who is a non-U.S. citizen do not qualify for the marital deduction on the decedent’s Federal Estate Tax return, form 709, and thus get taxed on the death of the spouse who is a U.S. citizen.

For a trust to qualify as a QDOT, the trust instrument requires that at least one trustee be a U.S. citizen or a domestic (U.S.) corporation and that no distribution of trust principal can be made unless that trustee has the right to withhold the tax imposed on QDOTs. A QDOT is authorized under the IRC §2056(d) and regulations thereunder governing the marital deduction for property passing to a surviving spouse.

A trust that is typically used to plan for asset transfer for the next generation is known as a “living trust” and is revocable and changeable during the lifetimes of the trust creators. If the trust creators (known as “Trustors” under trust law) have children and/or grandchildren the trust document will explain which children or grandchildren gets which assets and when.

A trust that is typically used to plan for asset transfer for the next generation is known as a “living trust” and is revocable and changeable during the lifetimes of the trust creators. If the trust creators (known as “Trustors” under trust law) have children and/or grandchildren the trust document will explain which children or grandchildren gets which assets and when. Is My Inheritance Taxable – Your inheritance of money or property may come from the estate of a deceased person or from a trust established previously. These types of things are generally referred to as “bequests” or “gifts” as far as tax law is concerned. People receiving bequests or gifts are referred to as “beneficiaries”.

Is My Inheritance Taxable – Your inheritance of money or property may come from the estate of a deceased person or from a trust established previously. These types of things are generally referred to as “bequests” or “gifts” as far as tax law is concerned. People receiving bequests or gifts are referred to as “beneficiaries”.

The term “irrevocable trust” is commonly used by estate lawyers and financial planners to describe a trust which is permanent and cannot be changed or revoked.

The term “irrevocable trust” is commonly used by estate lawyers and financial planners to describe a trust which is permanent and cannot be changed or revoked. The term “living trust” is commonly used by estate lawyers and financial planners to describe a trust which is established during a person’s lifetime and which is revocable and changeable.

The term “living trust” is commonly used by estate lawyers and financial planners to describe a trust which is established during a person’s lifetime and which is revocable and changeable.

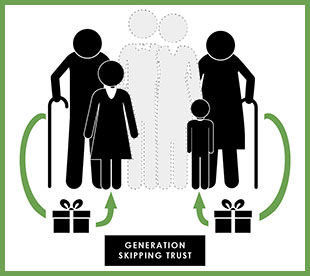

A Generation Skipping Trust (GST) is a generic term for any trust where there are trust benefits which are skipping a generation. A typical example is where a Trustor establishes a trust that does not benefit his children but instead benefits his grandchildren. Thus, the trust “skips” giving anything to the Trustor’s children. The law imposes a “Generation Skipping Tax” of a flat 40% on certain transfers above an exemption amount to insure that property transfers are subject to transfer tax at least once at each generation. The exemption amount is the same as the estate tax exemption amount which for 2014 is $5,325,000. The relevant IRC sections are §2601 through §2642.

A Generation Skipping Trust (GST) is a generic term for any trust where there are trust benefits which are skipping a generation. A typical example is where a Trustor establishes a trust that does not benefit his children but instead benefits his grandchildren. Thus, the trust “skips” giving anything to the Trustor’s children. The law imposes a “Generation Skipping Tax” of a flat 40% on certain transfers above an exemption amount to insure that property transfers are subject to transfer tax at least once at each generation. The exemption amount is the same as the estate tax exemption amount which for 2014 is $5,325,000. The relevant IRC sections are §2601 through §2642.