A living trust is one of the key ingredients in most estate plans. The living trust is widely used because of its flexibility. When people but their money and property into a living trust probate can be avoided and estate taxes saved.

Revocable Living Trusts – Creation and definition:

{kind=link}

The usual way for a single person to establish a living trust is to be the Trustor, the Trustee, and Beneficiary during his or her lifetime. Provision is also made for a successor Trustee to take over during the Trustor’s lifetime if the Trustor wants to resign from being a trustee or if the Trustor becomes incapacitated. The net effect is that the Trustor retains entire control and privacy over his or her financial affairs during lifetime since any successor Trustee is legally bound to follow the instructions of the Trust as to how to spend the Trust’s money.

A formal declaration of trust document is required to create a living trust and a formal transfer by deed or other transfer documentation must occur for each asset that is to be placed into the trust. The declaration of trust is the detailed roadmap as to how the trust matters are to be handled and as to how and when the trust income and assets are to be distributed. The declaration of trust in effect takes the place of a person’s will because assets transferred into the trust during the Trustor’s lifetime are not subject to any directions in the Trustor’s will. The following chart illustrates the different components and parties of a revocable trust.

TRUSTOREstablishes the Trust by transferring assets and bank accounts to the name of the Trustee THE TRUSTTrustee holds legal title and administers the assets and accounts according to the Trustor’s instructions in the Trust Declaration BENEFICIARIESReceive the income and asset distributions from the Trust. Trustor is usually the beneficiary during his or her lifetime.

Advantages/relationship to Will:

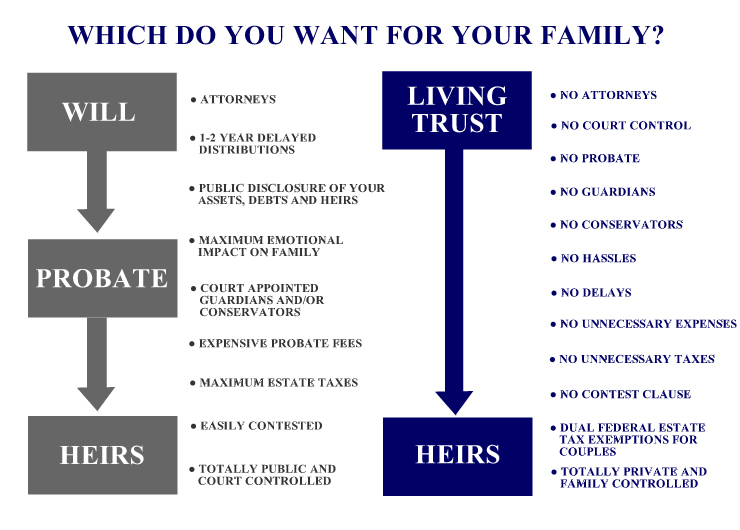

Revocable trusts are used primarily to avoid probate which has legally mandated fees. For example, probate fees on an estate of $1,000,000 are $20,000 for the attorney and $20,000 for the executor for a total of $40,000. The Revocable Trust also in effect serves as the Trustor’s will as far as how to divide up the trust assets at the Trustor’s death. Assets transferred into the Revocable trust are controlled by the trust and not by the Trustor’s Will. Also, in connection with establishing a Revocable trust, the Trustor will change his Will to provide that all assets not in the trust at death are to be transferred into the Revocable trust so that in effect his entire estate disposition is controlled by the trust. Other advantages include the avoidance of conservatorship and avoidance of will contest lawsuits.

{kind=link}

Income tax effects:

The income earned by the trust assets is generally taxed to the Trustor, and this type of trust is thus known as a “grantor trust” under the tax laws. This type of trust does not shift income away from the Trustor. For example, a Trustor owning stocks that pay dividends cannot shift the income from the dividends out of his personal taxable income by transferring the stock into the trust. All dividends or interest paid after the transfer date go onto the Trustor’s personal income tax return, form 1040, for tax purposes. Annual income tax returns are not required to be filed by a revocable trust, as long as the Trustor is alive, since the trust income is taxed to the Trustor.

Gift tax effects:

No gift tax is payable on transfers to a revocable trust since there is not a legally completed gift.

Estate tax effects/Tax basis on Trustor’s death:

Property transferred into a revocable trust is included in the Trustor’s estate for estate tax purposes at its date of death value. The trust assets are therefore included in the federal form 706 estate tax return. However the trust assets do then receive a step-up in income tax basis to the date of death fair market value, up to certain amounts. For example, a house purchased for $100,000 which is worth $500,000 as of the date of death could be sold by trust or the trust beneficiaries after the Trustor’s death for $500,000 and there would be no capital gains income tax. On the other hand, if that same house would have been sold by the trust before the Trustor’s death for $500,000, then the Trustor would have had to pay capital gains income tax on $400,000 in capital gains. The tax would be about $100,000 (15% federal and 10% state tax).

Use of a living trust does not typically save any estate taxes for a single individual.

Choice of Trustee:

Most people select themself, the Trustor, as the initial Trustee, and designate one or more people to be the successor Trustees upon their resignation, disability, or death. However, it is possible to have another person, such as a friend or an adult child, or an independent trust company, serve as the initial Trustee. The use of an independent trustee allows the Trustor to monitor the trustee’s administration during the Trustor’s lifetime. The size of the trust and the complexity of the assets involved need to be considered in choosing a trustee. As long as the trust remains revocable, typically while the Trustor is still alive, the Trustee can be changed by the Trustor for any reason at any time.

No Protection from creditor’s claims:

A living trust is not typically used as an “asset protection” device. A living turst is by law responsible for the debts of the Trustor and can be sued by a creditor of the Trustor for the Trustor’s unpaid debts.

CALL (949) 851-1771 to speak with Lawyer David L. Crockett

Conveniently located in Newport Beach near the John Wayne Airport

We are located near the Orange County California John Wayne Airport. My office is catty-corner from Fletcher-Jones Motorcars; —right behind the rear entrance of Newport Lexus on Dove Street. Here is a picture of my office building and a Google Map to get your bearings.